Annual Business Report: How to Write One

Learn how to write an annual business report that meets compliance requirements and communicates effectively. This guide covers structure, required sections, and step-by-step process.

Quick Verdict

An annual business report is a formal document that summarizes your company’s financial performance, operations, and strategic direction over a 12-month period. It’s created by leadership and finance teams, with input from across the organization, to communicate results and plans to stakeholders.

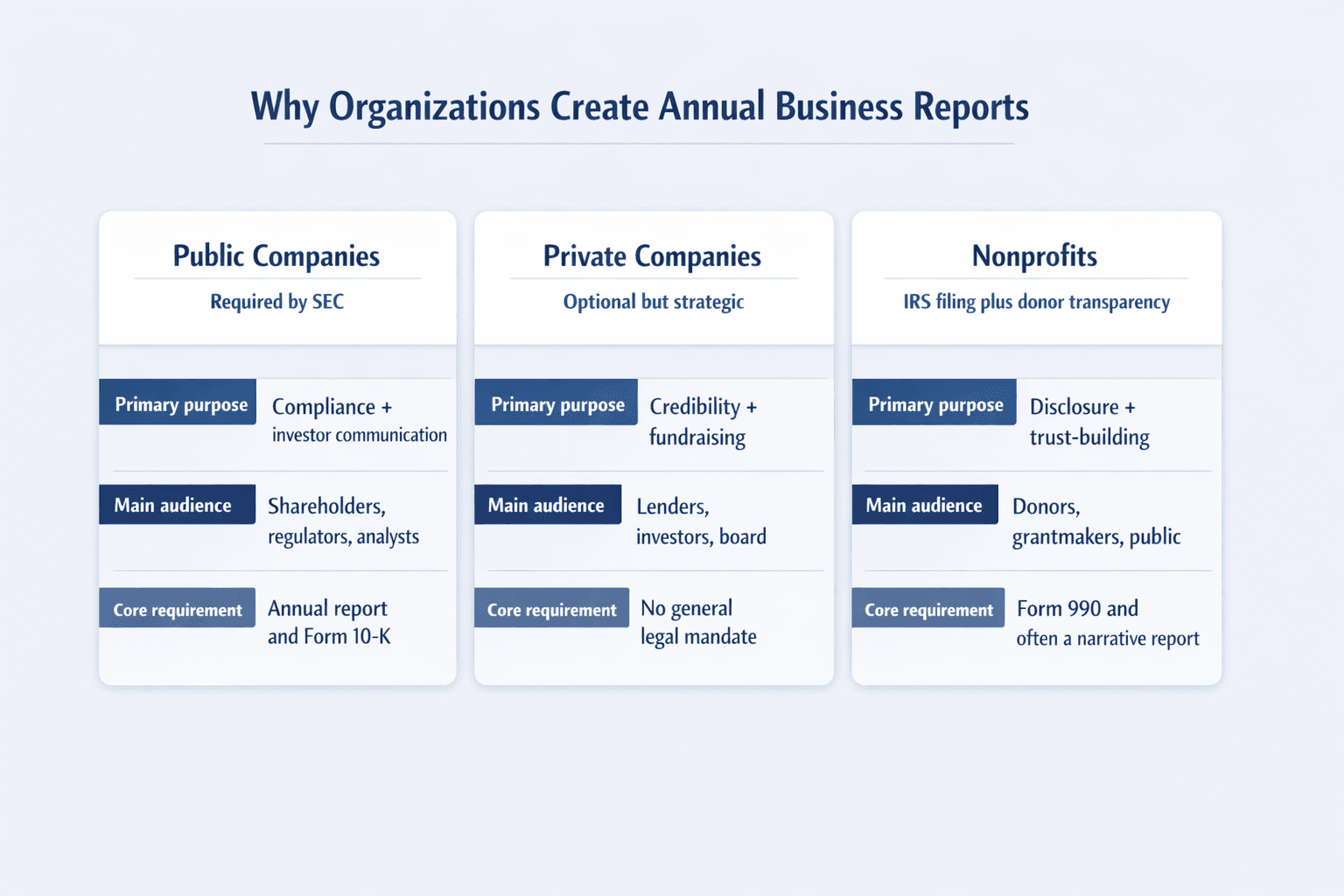

For publicly traded companies, annual reports are required by law—they must file detailed reports with the SEC and send them to shareholders. Private companies and nonprofits aren’t legally required to produce annual reports, but many do anyway to build credibility, attract investors, and maintain transparency with donors, board members, and employees.

This guide will teach you how to write an annual business report that meets regulatory requirements (if applicable) and effectively communicates your company’s story. You’ll learn what to include, how to structure each section, and how to avoid the most common mistakes that undermine credibility.

What Is an Annual Business Report?

An annual business report is a comprehensive document that details your company’s financial results, operational achievements, governance practices, and strategic outlook for a completed fiscal year.

It serves two purposes: meeting regulatory compliance requirements (for public companies and many nonprofits) and communicating transparently with all stakeholders—investors, employees, customers, donors, and the public—about your organization’s health and direction. The SEC requires public companies to send annual reports to shareholders when voting for directors, while tax-exempt organizations file Form 990 to satisfy IRS disclosure requirements.

Annual business reports typically include:

- Financial statements — Balance sheet, income statement, cash flow statement, and statement of shareholders’ equity

- Executive summary or letter to shareholders — High-level overview from CEO or board chair

- Management discussion and analysis (MD&A) — Leadership’s interpretation of results and business conditions

- Operational highlights — Major achievements, product launches, market changes

- Corporate governance information — Board composition, compensation, policies

- Future outlook and strategy — Goals, opportunities, and anticipated challenges for the coming year

Who Creates Annual Business Reports

Not every organization produces an annual business report—but many types do, either because they’re required by law or because it’s strategically valuable.

- Publicly traded companies — SEC regulations require public companies to file annual reports and distribute them to shareholders

- Private companies — No legal requirement, but annual reports build credibility with lenders, investors, and potential buyers

- Nonprofits — Tax-exempt organizations must file Form 990 annually, and many publish narrative annual reports for donors and the public

- Government agencies — Federal agencies produce annual performance and financial reports to demonstrate accountability and results

- Cooperatives and member organizations — Often required by bylaws or governance structures to report to members annually

Why Annual Business Reports Matter

Annual reports aren’t just paperwork—they’re strategic tools that serve multiple purposes.

- Regulatory compliance — Public companies must meet SEC filing requirements; nonprofits face IRS penalties and potential loss of tax-exempt status for repeated failures to file

- Stakeholder transparency — Investors, donors, and employees use annual reports to assess organizational health; some rely on these documents as their primary source of information

- Attracting investment — Comprehensive annual reports demonstrate maturity and professionalism to potential investors, lenders, and partners

- Building credibility — Public disclosure of finances, governance, and strategy builds trust with all stakeholder groups

- Strategic planning tool — The annual report process forces leadership to evaluate performance, identify trends, and articulate future direction

- Historical record — Annual reports create a permanent archive of your organization’s evolution, decisions, and results

Key Components of a Business Annual Report

Annual reports follow a fairly standard structure—public companies must include specific sections required by the SEC, and private companies typically adopt similar frameworks. Some sections are mandatory; others are strategic additions.

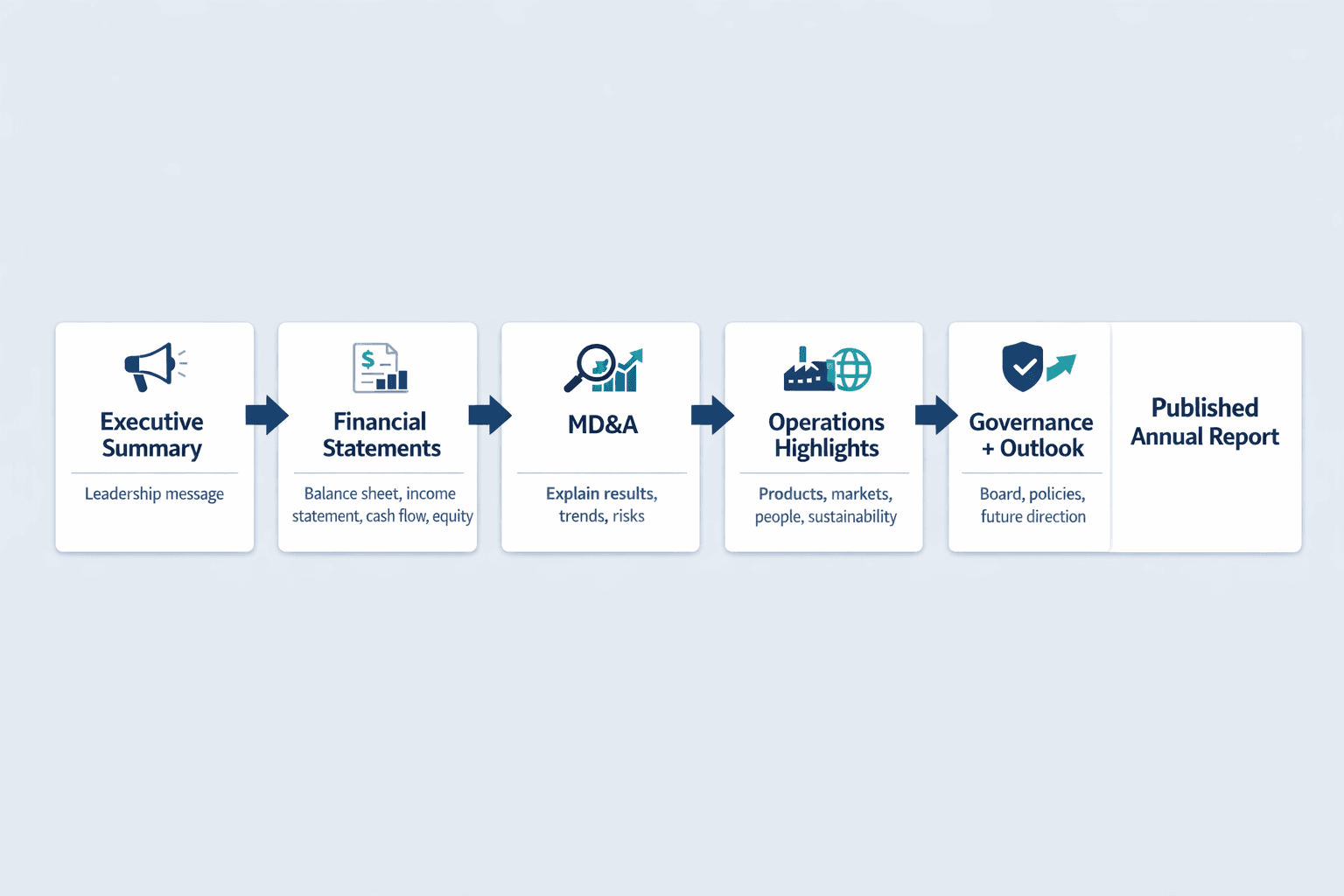

Executive Summary/Letter to Shareholders

The opening section is usually a message from your CEO or board chair that provides a high-level view of the year’s performance. This letter isn’t just for regulatory compliance—it’s your chance to communicate management’s perspective directly to readers who may not dig into the full report.

Include these elements in your executive summary:

- Major achievements — Highlight 2-3 significant wins, such as revenue milestones, product launches, or market expansion

- Financial highlights — Summarize key financial results in plain language (revenue growth, profitability, cash position)

- Strategic initiatives — Explain major decisions, investments, or pivots made during the year

- Challenges faced — Acknowledge setbacks or headwinds honestly—this builds credibility

- Future outlook — Preview your strategic direction for the coming year without overpromising

Because auditors review narrative sections for consistency with audited financial statements, keep your tone balanced—emphasize achievements, but don’t exaggerate or contradict the numbers.

Financial Statements

The financial statements form the core of any annual report. Public companies must present audited statements following U.S. GAAP or IFRS standards; private companies may use audited or unaudited statements depending on their stakeholder requirements.

Every annual report should include these four statements:

- Balance sheet — Shows assets, liabilities, and equity at fiscal year-end (your financial position at a point in time)

- Income statement — Displays revenues, expenses, and net income or loss (your operating performance over the year)

- Cash flow statement — Tracks cash generated and used in operating, investing, and financing activities (where cash came from and went)

- Statement of shareholders’ equity — Documents changes in equity accounts, including retained earnings, stock issuance, and dividends (how ownership value changed)

These statements must be prepared consistently using recognized accounting standards. Private companies sometimes combine or simplify these for readability, but the fundamentals remain the same.

Management Discussion and Analysis (MD&A)

The MD&A section gives management a chance to interpret the financial results—explain what happened, why it happened, and what trends or risks might affect future performance.

MD&A typically covers these topics:

- Revenue trends — Break down where revenue came from, which segments grew or declined, and what drove the changes

- Expense analysis — Explain major cost categories, year-over-year changes, and cost-control efforts

- Market conditions — Discuss how external factors (economy, competition, regulation) affected your business

- Operational changes — Describe significant operational decisions, such as facility openings, technology investments, or workforce adjustments

- Risk factors — Identify key risks that could impact future results (competitive threats, regulatory changes, supply chain issues)

- Forward-looking statements — Explain management’s expectations for the coming year, including growth opportunities and anticipated challenges

MD&A should be written in accessible language—you’re explaining your business to investors, not reciting accounting textbooks. Use concrete examples and year-over-year comparisons to make trends clear.

Business Operations and Highlights

This narrative section covers non-financial achievements and operational updates. It’s where you tell the story behind the numbers—what your company actually did during the year.

Common topics include:

- Product launches — New offerings, features, or service lines introduced

- Market expansion — Geographic growth, new customer segments, or distribution channels

- Employee initiatives — Workforce growth, diversity programs, training investments

- Sustainability efforts — Environmental programs, social responsibility, community involvement

- Technological improvements — System upgrades, digital transformation, operational efficiencies

Keep this section grounded in verifiable accomplishments. Because auditors check narrative sections for consistency with financial records, don’t make claims you can’t back up with data.

Corporate Governance

The governance section details your company’s leadership structure and ethical practices. Public companies must disclose directors, executive officers, and certain compensation information.

Standard governance disclosures include:

- Board of directors profiles — Names, backgrounds, committee assignments, and independence status

- Executive compensation — Salaries, bonuses, equity awards, and benefits for top officers

- Audit committee reports — Summary of audit committee activities and financial oversight

- Compliance policies — Code of ethics, whistleblower procedures, conflict-of-interest policies

- Shareholder rights — Voting procedures, proxy access, dividend policies

Even private companies benefit from governance transparency—it demonstrates professionalism and accountability to investors, lenders, and employees.

Future Outlook and Strategy

This forward-looking section outlines where your company is headed. It’s less about precise forecasts and more about communicating strategic direction and priorities.

Address these elements:

- Strategic goals — Your top priorities for the coming year (revenue targets, product roadmap, operational improvements)

- Market opportunities — Trends, customer needs, or competitive gaps you plan to capitalize on

- Planned investments — Major spending areas (technology, facilities, talent, R&D)

- Anticipated challenges — Risks or obstacles you expect to face and how you plan to address them

- Growth projections — High-level guidance on expected performance (be realistic—overpromising damages credibility)

Frame your outlook carefully. Forward-looking statements should be paired with risk factors to give readers a balanced view of possibilities and uncertainties.

How to Write an Annual Business Report: Step-by-Step Process

Creating an annual report isn’t a last-minute task. It requires planning, coordination across departments, and systematic execution—auditors review annual reports for consistency, and regulators expect timely, accurate filings.

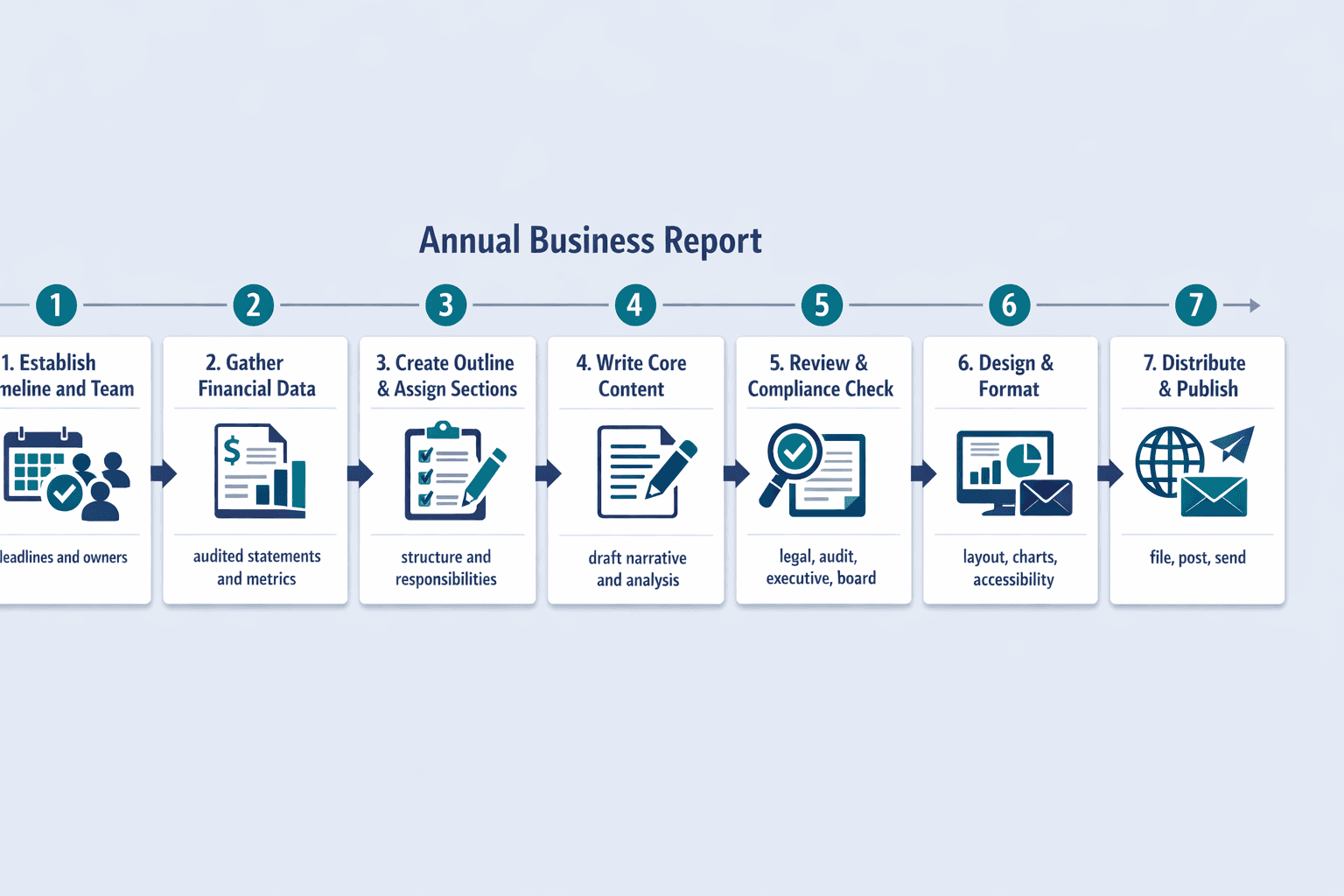

Step 1: Establish Timeline and Team

Start planning 2-3 months before your fiscal year-end. Public companies face strict deadlines—60 days for large accelerated filers, 75 days for accelerated filers, and 90 days for others—so you need sufficient lead time for drafting, review, audit, and approval.

Assemble a cross-functional team that includes:

- Finance team — Prepares financial statements, gathers metrics, coordinates with auditors

- Executive leadership — Writes or reviews executive summary, strategy sections, and MD&A

- Legal and compliance — Ensures regulatory requirements are met, reviews disclosures for accuracy

- Marketing and communications — Handles design, writing, and accessibility

- External auditors — Audits financial statements and reviews other information for consistency

- Board of directors — Reviews and approves the report before publication

Set internal deadlines for each section and establish a clear approval workflow—annual reports touch too many stakeholders to improvise the process.

Step 2: Gather Financial Data and Documentation

Annual reports are built on audited financial statements and supporting records. Start collecting documentation early—financial statements must be complete before you can finalize narrative sections.

Compile these materials:

- Audited financial statements — Balance sheet, income statement, cash flow statement, equity statement

- Operational metrics — Customer counts, employee headcount, units sold, transaction volumes

- Employee statistics — Workforce size, diversity data, turnover rates, compensation trends

- Customer data — Retention rates, satisfaction scores, major client wins or losses

- Market analysis — Competitive positioning, market share, industry trends

- Previous year’s report — For year-over-year comparisons and consistency checks

- Legal disclosures — Pending litigation, regulatory changes, compliance updates

The PCAOB requires auditors to confirm that supplemental information reconciles to financial statements or underlying records, so make sure your source data is traceable and accurate.

Step 3: Create Outline and Assign Sections

Break the report into manageable sections with clear ownership. Public-company reports follow a standard structure—Business, Risk Factors, MD&A, Financial Statements, Governance—which provides a good template even for private organizations.

Follow these organizational tips:

- Assign section owners — Each major section needs a clear author (CEO writes shareholder letter, CFO writes MD&A, legal writes governance)

- Set internal deadlines — Stagger section drafts so finance completes statements first, then MD&A, then narrative sections

- Establish word count or page limits — Prevents scope creep and keeps the report focused

- Define approval workflow — Specify who reviews each section and in what order (department head → legal → executive → board)

- Determine design and layout requirements — Decide early whether you need a professional designer or can handle formatting internally

If your report includes proxy-related governance disclosures, coordinate your annual report and proxy timelines—some companies split these across documents, others combine them.

Step 4: Write Core Content Sections

Now comes the actual writing. Each section should be clear, accurate, and aligned with your audited financials. The SEC emphasizes that MD&A should explain management’s view of performance and trends, not just recite numbers.

Follow these writing best practices:

- Use clear, accessible language — Write for investors and stakeholders, not accountants (define technical terms, avoid jargon)

- Balance positive achievements with honest challenges — Credibility comes from transparency, not spin

- Include specific data and examples — “Revenue grew 15% to $12M” is stronger than “Revenue increased significantly”

- Maintain consistent voice — The entire report should read like one cohesive document, even if multiple authors contributed

- Avoid jargon — Terms like “synergies” or “optimization” are vague—use concrete language instead

- Cite sources for external data — If you reference market research or industry statistics, link to the source

Because auditors check for consistency between narrative and financial statements, every major claim in your MD&A or business highlights should be reconcilable to underlying data.

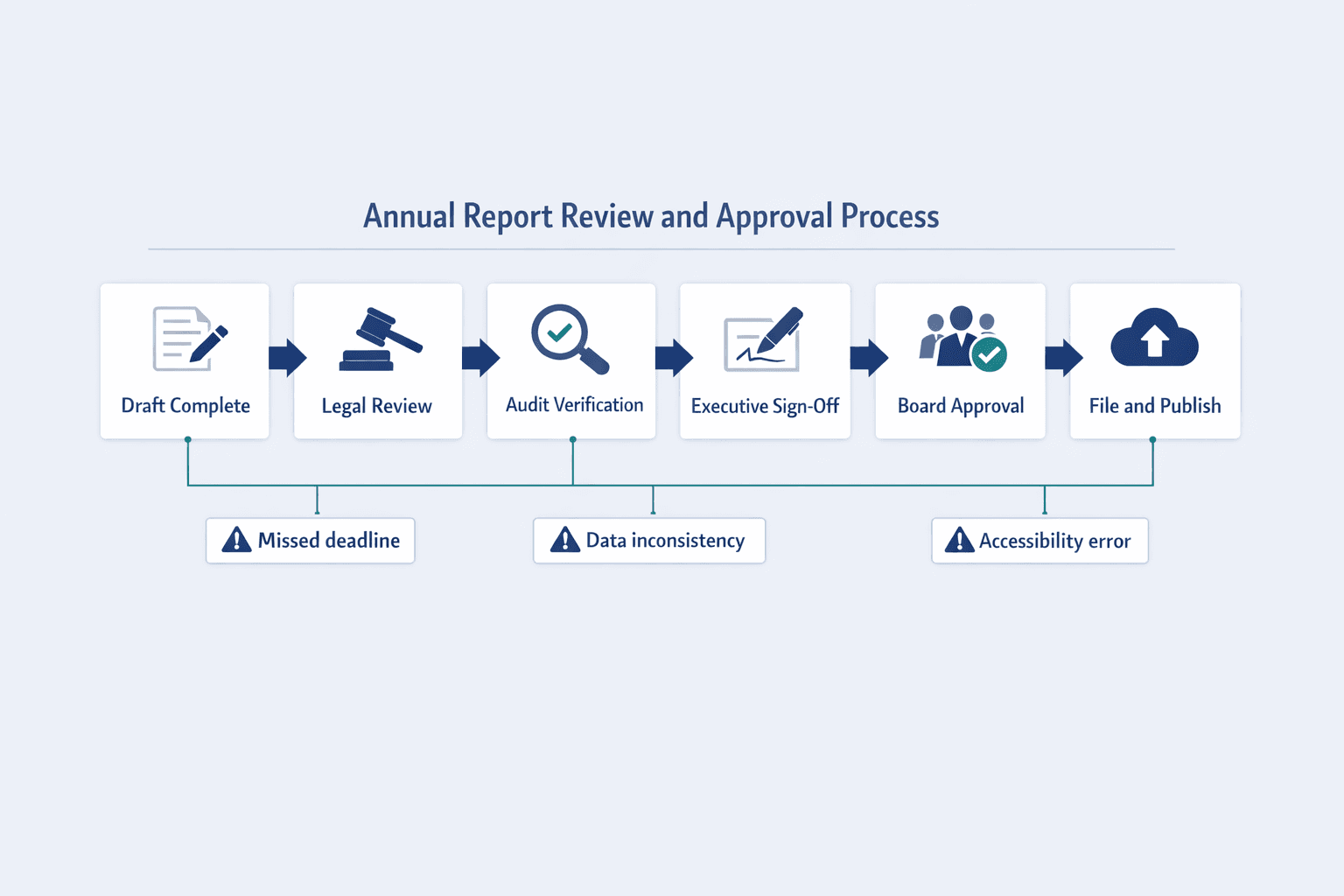

Step 5: Review and Compliance Check

Once drafts are complete, launch a thorough review process. Auditors read annual reports for material inconsistencies, and regulators scrutinize compliance with disclosure rules—errors can have legal and financial consequences.

Structure your review in stages:

- Legal review for compliance — Confirm all required disclosures are present and accurate (especially important for public companies)

- Financial audit verification — Auditors confirm financial statements and check that supplemental information reconciles to accounting records

- Executive approval — CEO, CFO, and other executives review and sign off on the report

- Board review — Board of directors reviews and formally approves the report before filing or publication

- External counsel review — For public companies, outside legal counsel often provides a final compliance check

Don’t skip the cross-check between narrative and financials. If your MD&A says revenue grew 15% but the income statement shows 12%, auditors will flag the inconsistency.

Step 6: Design and Format

Visual presentation matters. A well-designed annual report is easier to read, more professional, and more accessible to diverse audiences. Accessible PDFs must be tagged to meet Section 508 standards.

Design considerations include:

- Consistent branding — Use your company’s fonts, colors, and logo throughout

- Professional layout — Employ clear typography, adequate white space, and logical section breaks

- Charts and graphs for data visualization — Complex financial data is more digestible as visuals (revenue trends, expense breakdowns, year-over-year comparisons)

- Accessible formatting — Create tagged PDFs with proper heading structure, alt text for images, and screen-reader compatibility

- Navigation aids — Include a table of contents, page numbers, and section headers for easy reference

- High-quality images — If you include photos, use professional-quality images that reflect your brand

Test your final PDF for accessibility—ensure headings are properly tagged, links work, and the document is readable with assistive technology.

Step 7: Distribute and Publish

Once your report is finalized and approved, distribute it according to legal requirements and stakeholder expectations. Public companies must file Form 10-K within 60-90 days of fiscal year-end, depending on filer status.

Distribution channels include:

- SEC filing — Public companies file Form 10-K or combined annual report via EDGAR

- Company website — Post the report prominently on your investor relations or about page

- Shareholder mailing — Send printed or digital copies to shareholders in connection with annual meetings and proxy materials

- Investor relations portal — Upload to your IR platform for easy stakeholder access

- Press release announcement — Notify media and key stakeholders when your annual report is published

For nonprofits, Form 990 must be made available for public inspection for three years—post it clearly on your website to meet disclosure obligations.

Annual Business Report vs. Other Business Documents

Annual reports aren’t the only documents companies produce—and they differ from quarterly reports, business plans, and other corporate communications in purpose, audience, and detail level.

| Document Type | Purpose | Audience | Frequency | Level of Detail | Legal Requirements |

|---|---|---|---|---|---|

| Annual Report | Comprehensive year-end summary of financial and operational performance | Shareholders, investors, regulators, public | Once per year | High—includes full audited financials, MD&A, governance | Required for public companies and many nonprofits |

| Quarterly Report (10-Q) | Update on financial performance for one quarter | Shareholders, investors, analysts | Four times per year | Moderate—interim financials, MD&A for the quarter, but less comprehensive | Required for public companies |

| Business Plan | Strategic roadmap for growth and operations | Internal leadership, investors, lenders | Updated as needed | High—detailed projections, market analysis, but focused on future plans | Not legally required; used for fundraising and planning |

The key difference: an annual report is backward-looking (what happened last year) plus interpretive (what it means for the future). A business plan is almost entirely forward-looking and strategic. A quarterly report is a shorter interim update on recent performance.

Common Mistakes to Avoid

Even experienced companies make annual report errors that reduce credibility or create compliance issues.

- Missing deadlines — Public companies face strict filing deadlines, and nonprofits risk tax-exempt status for repeated failures to file on time

- Burying important information — Don’t hide bad news in footnotes or dense paragraphs; readers will find it anyway, and transparency builds trust

- Inconsistent data across sections — Auditors flag material inconsistencies between narrative claims and audited financials

- Overly promotional tone — Annual reports should inform, not sell; exaggeration undermines credibility

- Ignoring negative results — Acknowledge challenges honestly and explain how you’re addressing them

- Poor visual design — Dense text blocks, inconsistent formatting, and inaccessible PDFs make reports hard to read

- Lack of forward-looking content — Readers want to know where you’re headed, not just where you’ve been

- Insufficient proofreading — Typos, broken links, and formatting errors look unprofessional and raise questions about attention to detail

If you’re legally required to file an annual report, the cost of missing deadlines or filing inaccurate information far exceeds the cost of doing it right the first time.

Annual Report Best Practices

Exceptional annual reports share a few characteristics that set them apart from adequate ones.

- Start with a strong executive summary — Give readers the highlights upfront; most won’t read the entire report

- Use data visualization effectively — Charts and graphs make trends more digestible than tables or text

- Tell compelling stories alongside numbers — Pair financial results with real examples (customer wins, employee achievements, operational improvements)

- Be transparent about challenges — Acknowledge risks and setbacks honestly; readers respect candor more than spin

- Highlight strategic vision — Explain not just what happened, but why it matters and where you’re headed

- Make it accessible to non-financial readers — Define terms, minimize jargon, and write in plain language

- Include year-over-year comparisons — Context matters—show how this year compares to last year to highlight trends

- Provide clear contact information — Make it easy for stakeholders to reach investor relations, board members, or leadership with questions

Current reporting practice shows that sustainability and long-term risk discussions are increasingly expected—even when not legally required—so addressing nonfinancial issues strengthens your report.

Tools and Resources for Creating Annual Reports

Various software tools and professional services can streamline the annual report creation process—but the right choice depends on your organization’s size, complexity, and compliance requirements.

Report Design Software

- Adobe InDesign — Professional page layout and design for polished, print-ready reports

- Microsoft Word — Sufficient for straightforward reports with basic formatting needs

- Canva — User-friendly design tool suitable for small businesses without dedicated designers

- Specialized financial reporting software — Tools like Workiva or Certent automate data linking and version control

- Presentation tools — PowerPoint or Google Slides work for simple digital-only reports

Whichever tool you use, ensure your final PDF is accessible—properly tagged with headings, alt text, and navigable structure for screen readers.

Financial Reporting Tools

Annual reports center on audited financial statements, so your accounting and analysis tools need to produce reconciled, reviewable outputs.

- Accounting software with reporting features — QuickBooks, Xero, NetSuite, or similar platforms for core financials

- Spreadsheet programs — Excel or Google Sheets for data analysis, year-over-year comparisons, and MD&A preparation

- Business intelligence platforms — Tools like Tableau or Power BI for visualizing financial and operational data

- Audit management systems — Software that facilitates auditor access to supporting documentation and reconciliations

PCAOB standards require that supplemental information reconcile to financial statements or underlying records, so use systems that maintain clear data trails.

Professional Services

External expertise often improves quality and reduces risk—especially for complex organizations or first-time report writers.

- Financial auditors — Public companies must use auditors to examine financial statements and review accompanying information

- Corporate communications consultants — Help draft narrative sections, shareholder letters, and MD&A in accessible language

- Graphic designers — Create professional layouts, charts, and branding for reader-friendly reports

- Legal compliance advisors — Confirm that disclosures meet SEC requirements and other regulatory obligations

Investing in professional services reduces the risk of errors, compliance failures, and stakeholder confusion—issues that cost far more to fix after publication.

Frequently Asked Questions

How long should an annual business report be?

There’s no legally mandated page length for an annual report. Public-company reports can be lengthy because Form 10-K requires detailed disclosures across multiple sections—many range from 50 to 150 pages. Private companies and nonprofits often produce shorter reports (20-50 pages) focused on key financials, highlights, and strategy.

The right length depends less on page count and more on whether you’ve clearly covered core sections—audited financial statements, management analysis, governance, risks, and forward direction—without unnecessary filler or repetition.

When are annual business reports due?

Public companies must file Form 10-K within 60 days of fiscal year-end for large accelerated filers, 75 days for accelerated filers, and 90 days for all others. For nonprofits, Form 990 is due by the 15th day of the fifth month after tax year-end—May 15 for calendar-year organizations.

Private companies typically set their own timeline unless lenders, investors, or governance policies impose a deadline. Start planning 2-3 months before year-end to allow sufficient time for drafting, audit, review, and approval.

Who is the audience for annual business reports?

Annual reports serve multiple stakeholder groups. For public companies, the primary audience is shareholders and prospective investors, especially in connection with annual meetings and proxy voting. For nonprofits, the IRS notes that some rely on Form 990 as their primary source of information about an organization—meaning donors, journalists, watchdogs, and grantmakers are key readers.

Other important audiences include employees (who want to understand company health), lenders (assessing creditworthiness), financial analysts (evaluating investment potential), regulators (confirming compliance), and customers or partners (gauging stability).

Do private companies need to create annual reports?

No—private companies are generally not subject to SEC annual report requirements unless they’re reporting issuers. However, many private companies voluntarily create annual reports to communicate with boards, major investors, lenders, employees, or potential acquirers.

Even when not legally required, annual reports demonstrate organizational maturity, build stakeholder confidence, and create a valuable historical record. If you’re pursuing outside funding, preparing for acquisition, or answering to a board, an annual report is often worth the effort.

What's the difference between an annual report and a 10-K?

The SEC explains there’s overlap between the two, but they’re not identical. The Form 10-K is the SEC-required legal filing with prescribed disclosure items and strict compliance standards. The shareholder annual report is often more designed, reader-friendly, and narrative-focused—distributed with proxy materials to shareholders.

Some companies effectively combine the two by using a 10-K-based annual report package. Others keep the glossy annual report separate from the EDGAR filing. Either approach works—just ensure you meet all regulatory requirements.

Can annual reports be digital-only?

Yes. The SEC’s website-access rules support digital distribution—companies subject to accelerated filing deadlines must disclose where investors can obtain free online access to reports. Increasingly, organizations publish interactive web versions alongside or instead of printed copies.

Digital-only reports are acceptable as long as they’re accessible—properly tagged PDFs with navigable structure, alt text, and screen-reader compatibility. However, confirm any investor, regulator, grantmaker, or governing-document requirements for physical delivery or archived copies before going fully digital.